President Donald J. Trump marked the first official trading day for “Trump Accounts” on Monday by ringing a ceremonial opening bell in the Oval Office, joined by leaders from the New York Stock Exchange and Nasdaq.

The event gave the new children’s investment program a high-profile launch. For families, however, the more important news is that Trump Accounts are now open, contributions have begun, and eligible children may qualify for a $1,000 federal contribution.

Trump Accounts are tax-advantaged investment accounts created for children in the United States. The accounts are designed to give children early exposure to the stock market and help families begin building long-term savings for the next generation.

The program was created under President Trump’s Working Families Tax Cuts Act, part of the broader One Big Beautiful Bill agenda. Supporters have described it as part of an effort to give more American families a direct ownership stake in the country’s economic growth.

The biggest immediate benefit is the $1,000 Treasury contribution. Eligible U.S. citizen children born between January 1, 2025, and December 31, 2028, can receive the one-time federal contribution. The child must have a valid Social Security number.

Families with older children should note an important distinction: Children under 18 may generally have Trump Accounts opened for them, but the $1,000 federal pilot contribution is limited to children born during that four-year window.

Parents and guardians who want to open an account must begin with IRS Form 4547, officially titled “Trump Account Election(s).” The form is used to elect to open a Trump Account and, when the child qualifies, to request the $1,000 pilot contribution.

The election can be made with a federal tax return, through the online Form 4547 portal, or by paper filing according to IRS instructions. Families will need the child’s Social Security number, date of birth, and other identifying information.

Parents should not assume the $1,000 will appear automatically. For children who qualify, the authorized adult must make the election and request the pilot contribution.

After the election is processed, Treasury or its agent sends activation information to the authorized individual. Treasury has said families should use TrumpAccounts.gov or the official Trump Accounts app to complete setup, view balances, and manage the account.

Families should also be careful about scams. Because the program involves children, Social Security numbers, and a federal benefit, parents should avoid links in suspicious emails or text messages and use only official channels.

Once the account is activated, parents, grandparents, relatives, friends, employers, charities, and other eligible contributors may be able to add money, subject to the rules of the program. In general, private contributions are capped at $5,000 per year per child. Employers may contribute up to $2,500 per year, counted toward that same annual limit.

The accounts are managed by parents or guardians while the child is a minor. The funds generally cannot be withdrawn before January 1 of the calendar year in which the child turns 18. After that, the account is treated under traditional IRA rules, including applicable tax treatment and exceptions.

At launch, cash contributions are automatically invested in the State Street SPDR Portfolio S&P 500 ETF, known by the ticker SPYM. The fund tracks the S&P 500 and gives children broad exposure to the U.S. stock market. Treasury has also selected low-cost index options from Vanguard and BlackRock’s iShares, with additional investment-election features expected later.

That means the account is not the same as a regular savings account. The money is invested, and investments can rise or fall. Families should understand that there is market risk. At the same time, children have one major advantage adult investors do not always have: time. A child who begins investing early may have many years for contributions and market growth to compound.

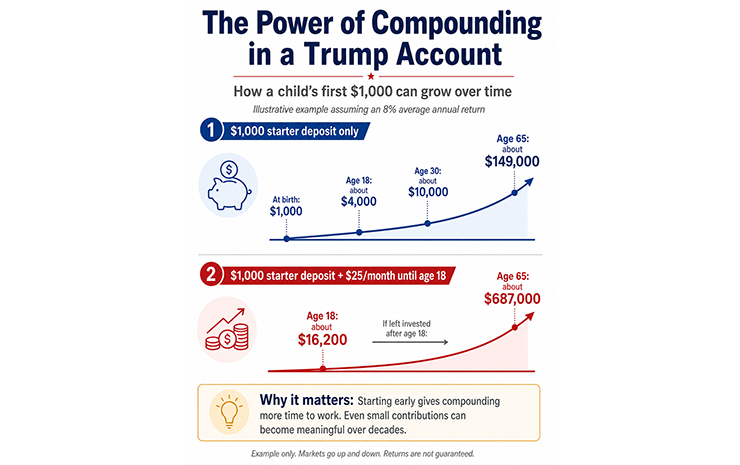

A simple example shows why starting early matters. If a $1,000 deposit grows at an average of 8 percent a year, it would become nearly $4,000 by the time a newborn turns 18, about $10,000 by age 30, and almost $150,000 by age 65, even if the family never adds another dollar. If parents or grandparents add just $25 a month until the child turns 18 and then stop, the account could grow to more than $16,000 by age 18 and, if left invested, could become hundreds of thousands of dollars by retirement age.

For many families, the $1,000 seed contribution will be only the beginning. Grandparents can contribute for birthdays. Parents can set up small recurring contributions. Employers may eventually offer Trump Account contributions as a benefit for workers with children. Community organizations and philanthropists may also use the accounts to help children who would otherwise not receive regular investment contributions.

The Treasury Department selected BNY as financial agent to support the program’s infrastructure. BNY partnered with Robinhood, which Treasury says will serve as the brokerage and initial trustee. The app and website are expected to include balance tracking, contribution tools, investment information, and financial education features.

The program has already attracted major private-sector support. Michael and Susan Dell committed $6.25 billion to provide $250 to 25 million eligible American children age 10 and under, including children born from 2016 through 2024. That pledge is aimed at children who are outside the federal newborn pilot window.

At the White House event, Treasury Secretary Scott Bessent said Trump Accounts are meant to help create “an ownership economy where all citizens become shareholders.” He said many American families still have no exposure to the stock market and argued that the program could help change that over time.

For parents, the practical takeaway is clear: Check whether your child qualifies, file the required election, claim the $1,000 if eligible, and decide whether regular contributions make sense for your family.

By Shabsie Saphirstein